Are P2P bloggers the worst investors?

Are P2P bloggers the worst investors?

100% of them lost money in Keutzal or Envestio or both.

5 days ago I had a look at P2P blogger portfolios after Keutzal was shut down. The picture was not pleasant: 68% of them lost money.

I predicted that more platforms would shut down, but had no idea everything would burn down so fast. Since then Envestio has deleted their website, blog and some social profiles, so I think it is safe to assume - they won't be back soon.

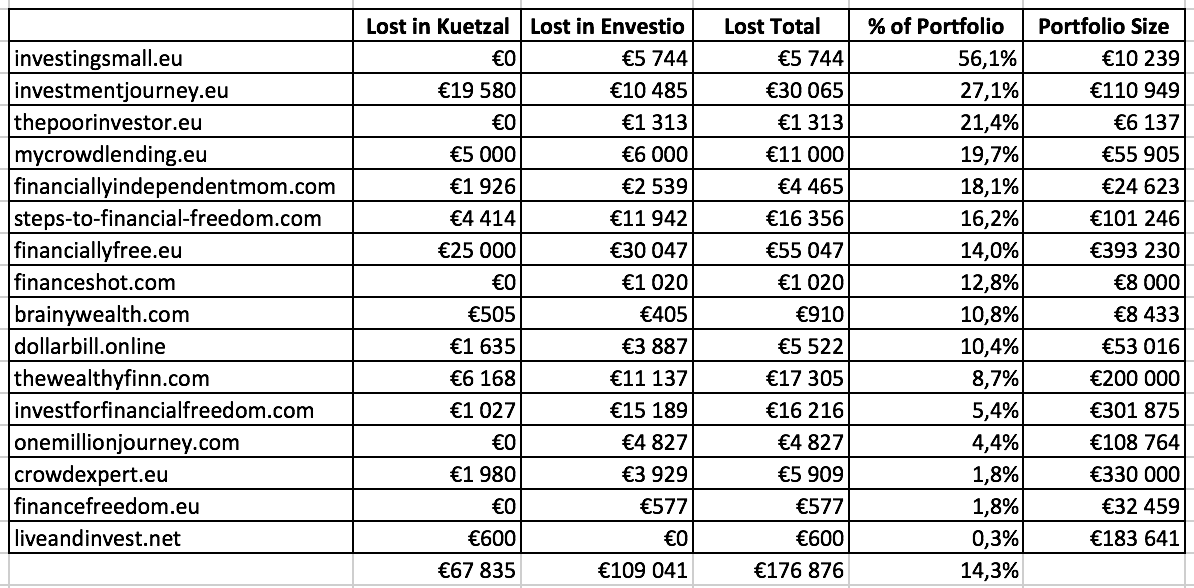

So how are P2P bloggers doing? Worse than I thought. 100% of the P2P bloggers have suffered losses either in Kuetzal or in Envestio, or both:

The average P2P blogger has lost 14% of his portfolio, and the biggest loss in terms of capital is achieved by Jørgen Wolf: 55 047 EUR.

Can we learn anything from this? I reached out to P2P bloggers and asked them following questions:

Keutzal and Envestio have shut down.

1. Any lessons learned?

2. Any changes to portfolio planned?

Thank you to all who cared to respond! See answers below:

The Wealthy Finn:

Lessons learned?

Buyback guarantees are a bad idea, if it means you can sell your investment back - even with a discount. I'm going to avoid such platforms.

Changes to portfolio?

Probably. I'll focus more on consumer loans and real estate than P2B. And those too likely with more caution than until now. Stocks, while over-priced, probably will get a larger share than they now have.

My Investment Journey

Lessons learned?

I'm trying to take all this as a big and expensive lesson learned. The main lesson learned is, don't be naive, be sharper in my own due diligence. Quite frankly I dismissed platform risk way too quickly during my own assessment. I was always fully prepared for default risk of certain loans on P2B platforms, but I heavily underestimated platform risk. If you can't verify the basics, don't risk your capital to begin with. Mentally I've written off my Kuetzal and Envestio portfolio completely.

Changes to portfolio?

I'm re-thinking my P2P allocation. Obviously, I'll be taking a closer look at my P2B portfolio. However, given the buyback freeze at Monethera and Wisefund, there is not a lot I can do at this very moment. For the very short term I plan to hold off on further P2B investments with TFGCrowd, Monethera and Wisefund and increase my stake with Mintos.

Investing small

Lessons learned?

High risk is part of P2P as it is and was for crypto. Probably you also have been burnt back in the beginning of 2018.

However, I must say and I think you will agree with me, that in investing there is only one free lunch - diversification. This is why I chose 5 platforms from the very beginning of my first investment back in 2018.

Question yourself and others and learn from your own and other's mistakes. This is no newcomer but would like to remind everyone - never invest more than you can afford to lose, no matter how tempting the yield.

Changes to portfolio?

For me it is too early to say. I will wait and react according to the situation - pragmatically like I feel I have done before. I closely follow Telegram group developments. If it all goes to court, let us see it through. One thing is can not be emphasised enough, diversification is the way forward. As Latvians have a saying "the manure must be scattered for better yield". The same goes for the money.

FinanceShot

Lessons learned?

Well, I knew that this was a very risky investment, so I'm not so surprised. Indeed I deposited only a very little % of my Portfolio on Envestio. Then my balance became bigger, but my deposit was little. However, I learned to put even more attention while choosing where to invest.

Changes to portfolio?

For the moment I'll keep the same Portfolio, I just decided to limit the amount of money on every platform. For example, let's take Mintos. Every time my balance goes over 1000€ let's say, I withdraw the difference to go back to 1000€ and save that money for less risky investments (ETFs...)

Brainy Wealth

Lessons learned?

The crowdlending sector is in a crisis. Why? Kuetzal didn’t create the crisis. Compared to the sector Kuetzal wasn’t that ”huge”. The investors is creating the crisis. After the Kuetzal crash, the investors lost trust to the crowdlending platforms. And they are now taking advantage of early exit option. We ”the investors” overwhelmed Envestio, Wisefund and Monethera.

All platforms offers the early exit option, however, both Wisefund and Monethera are hit by the investors choosing to use it. Therefore they’ve disabled it. It seems worrying to me, that they can just go ahead and disable it, but that’s for another day.

Crowdestor might not have thought about this, but their buyback fund is a good concept, because we the investors cannot trigger it.

I don’t blame anybody for using the early exit function – the firms gotta do damage control, but we also need to.

Changes to portfolio?

Well I’m looking at my portfolio now and what I see quite a few high risk platforms which add up to more than it should. My portfolio is well Diversified, but it doesn’t matter when quite a few platforms are high risk and have a large stake. Nevertheless, no changes will be made to my portfolio yet. I’m waiting for the market to stabilize or just slow down and then I will play my cards.

Like stocks, we are now scared and I think the crowdlending sector will feel this, untill the trust is yet again build.

ThePoorInvestor

Lessons learned?

The overall transparency provided by the platforms has to be very evident. In the future platforms not stating loan originators will not be in my portfolio. High interest also involves high risk, but this was a given. I will preferably have loan agreements publicly available (like at Grupeer and Mintos). Personally I will properly use google maps (street view) to identify the physical location of the businesses or development projects. If the business or development project is legit, it should be no problem to find on google maps (street view). The google maps (street view) will be used to check if the signs has the name of the borrowing business and if the pictures provided by the platform is identical to what can be found on google maps.

Changes to portfolio?

Before all this panic, I started to withdraw money from Fastinvest and Envestio. The Envestio withdrawal was initiated in the middle of January and I have not yet received the payment (cannot remember the date, and cannot access envestio.com to check). Furthermore, I have withdrawn all my funds from Fastinvest. If you look back at my monthly updates, I have previously stated that the lack of loan originators transparency makes me uneasy. As a part of the new year, I was going to reevaluate my portfolio in P2P lending. One was to limit the obvious risk, such as the high interest rates with little transparency from Envestio (lacking public shown loan agreements and public showing the borrowing companies financials and actual existence).

Steps to Financial Freedom

Lessons learned?

I thought scammers would be reluctant to meet investors/bloggers in person, but I now now that is not the case. I met Kuetzal (Alberts Cevers and Romans Antonovs) in Riga, in a small office. In hindsight the small team and small office could have been red flags.

Now I think that a small team and small office indicates a risk: I think it is more difficult to uphold a scam when the team is very large. The more people are involved, the higher the probability the scam will be revealed. This is something I will actively investigate from now on. I will also have a closer look at the office spaces during my visits.

Besides that, I have been too blinded by the high (promised) return rates. Higher interest rates come with higher risks, and you should always spread your risk and diversify. I have added a lot of platforms to my portfolio, but invested a large part in the high-return platforms (20 platforms, but 11% of portfolio invested just in Envestio). I should be more satisfied with platforms with return rates of 10-14%, and invest small portions in high risk platforms.

Changes to portfolio?

I will move funds from platforms promising 15+% interest rates to platforms that feel safer (10-14% interest rates) and that have a longer proven track record (in existence for several years). I will still invest in the higher risk platforms but will limit this: max 2.5-5% of my total portfolio value per platform.

Dollarbill

Lessons learned?

It feels a bit like the early crypto days. A number of sincere initiatives, but unfortunately also a number of fraudulent altcoins initiatives. The good thing is that this makes the market more mature, the bad thing is that early investors lose a lot of money. Kuetzal is a different case than Envestio in that regard. Kuetzal was a youngster and had not yet proven himself. I attribute more recent developments around Envestio to the snowball effect (which bloggers, including me, are unfortunately also part of). It is a bank run, even any real bank anywhere in the world would get into serious trouble when this happens (everyone will probably remember the days in 2008 when we were very close to that moment) That is also the reason that a large part of my assets are in real assets (mainly precious metals) and not in a fiat money system, and are therefore a hedge against the current financial system.

Changes to portfolio?

From the start my intention was to spread my assets over as many platforms as possible and as many projects or loans as possible within a platform. In addition, platforms with high and lower risk and various assets (p2p loans, p2b loans and real estate). This approach has pros and cons. The advantage is that when a platform falls over, the loss remains limited, the disadvantage is that the chance of a platform falling over where you have invested increases. Answer to the question: since I see what is going on in the p2p market as a harbinger of our entire current financial system (which in fact is only based on trust) and exists by the grace of debt, I was already finishing my stock portfolio to build and convert to precious metals and bitcoin. For the p2p part, a larger share will go to the somewhat more traditional p2p loans with a short duration (such as peerberry, grupeer, mintos, swaper) and preferably to platforms with a healthy parent company. In addition, I still have faith in the real estate market for the next two years, especially for the rental variant. Passive income remains an important part, in addition to the hedge on the financial system as a whole.

As we can see, the average P2P blogger has managed to lose in 1 week about the same amount of capital they would earn in 1 year from interest payments. There are more suspicious platforms and the total losses probably will go up, but there are some good signs as well - bloggers are becoming more skeptical, want to do more due diligence and consider avoiding platforms that are not transparent.

Key takeaways

If you did not lose money in Keutzal and Envestio, you can consider yourself being a better investor than any of the 16 P2P bloggers reviewed

Not losing money is more important than getting higher interest

Due diligence must be done before doing an investment. Many had some suspicions about Kuetzal already a month before shutdown, and in case of Envestio - couple of weeks before shutdown, but that was too late

Most P2P platforms are not regulated, can change their terms any time. Make sure you completely trust them and better be on safer side than ignoring “red flags“.

Diversification does not work, if you diversify by investing in scams. Investing in 1 failed platform or 10? Result will be the same. Focus on safety & quality first, diversification second.

Want to get access to exclusive content? Become a paid subscriber:

Or join “High-risk investments“ Telegram group for an informal discussion.

Really good read. I noticed that many sunshine blogs have stopped. I´m quite sure we haven´t seen the end of drama.

Personally I think the next big thing will be Crowdestor.

Fondue.blog answers:

> Any lessons learned?

Don't be the dumb money. I will start a series of technical due diligence in the platforms, their hosting providers, their DNS registrations and their available linkedin profiles.

> Any changes to portfolio planned?

Disqualified some suspicious platforms for the second round of investments.